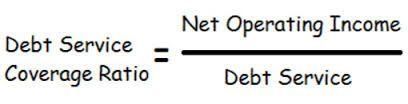

Given this, your focus should be on the Debt Service Coverage Ratio of the investment property when putting together a loan proposal. It’s a fairly straight-forward calculation – here is how this metric is estimated:

Imagine a small apartment building with four units where each unit rents for $1125. That’s a gross annual income of $54,000. Reduce that income by 5% for vacancy and credit loss to arrive at a GOI of $51,300.

Next, let’s calculate the Net Operating Income. For this example, let’s assume utilities, taxes, monthly and annual maintenance costs combine for total annual operating expenses of $27,281. You then subtract this amount from your GOI:

$51,300 (GOI) -$27,281 (Operating Expenses) = $24,019 (NOI)

Now we factor the annual debt service. For this example, let’s assume principal and Interest on a $350,000 loan at 4.1% for 30 years which yields an annual debt service of $20,016. Now, let’s calculate the Debt Service Credit Ratio:

$24,019 (NOI) -$19,998 (P&I) = 1.20 (DSCR)

In our example, this property with this income, expenses and loan costs would yield a Debt Service Credit Ratio of 1.20. What does this mean? This property will generate 20% more income than it needs to make its mortgage payments. For most commercial lenders, this would be a minimum amount they would normally accept as DSCR.

Cardinal Business Financing, Inc. is affiliated with only the top commercial lenders in the country. We are dedicated to finding the best financing and lending solutions of owners and investors of commercial real estate.

Please call us at (866) 578-5999 x101 to discuss your next equipment acquisition, or fill out our

Contact Us

form.

The post

What is DSCR? How Does It Affect Commercial Loan or Refinance Proposals?

appeared first on

Cardinal Business Financing, Inc.

.